Navigating the world of credit can be daunting, especially if you’re just starting out or looking to rebuild your credit. Fortunately, co-signed loans offer a powerful solution for individuals in these situations, providing access to funds they might not qualify for on their own and the opportunity to boost their credit score through regular repayments.

In this section, we’ll delve into the fundamentals of co-signed loans, their mechanics, and their role in building credit. From understanding what co-signed loans are to their impact on credit scores, we’ll cover everything you need to know about this financial tool.

What are Co-signed Loans?

A co-signed loan is a financial arrangement involving two parties: the primary borrower and the co-signer. This setup is typically used when the primary borrower’s credit history isn’t strong enough to secure a loan independently.

The co-signer, often someone with a better credit score and financial stability, agrees to back the loan, reducing the risk for the lender and increasing the borrower’s chances of loan approval.

Co-signer vs Co-borrower

When thinking about co-signed loans, it’s crucial to understand the roles of a co-signer and a co-borrower. They both help you get a loan but in different ways.

A co-signer steps in to help you qualify for a loan by promising to pay back the money if you can’t. However, they don’t have any ownership of what you’re purchasing with the loan. They’re there to reassure the lender that the loan will be repaid.

Conversely, a co-borrower shares ownership of the loaned money or assets and is equally responsible for paying back the loan. Unlike a co-signer, they’re directly involved in using the loan for its intended purpose.

The main differences lie in their financial responsibility and ownership rights. A co-signer acts as a safety net for payments, while a co-borrower is fully committed from the beginning. Also, if things go wrong, co-borrowers have a legal claim to what was purchased with the loan, whereas co-signers don’t.

Understanding these distinctions is essential when considering who to involve in your co-signed loan agreement.

Types of Co-signed Loans

Co-signed loans can be utilized for various purposes, including:

- Student loans: These loans are for covering higher education costs like tuition, books, and living expenses. Students with limited credit or income often need a co-signer, commonly parents, to help them qualify for the loan.

- Auto loans: They finance vehicle purchases, new or used. Co-signers can join to improve approval chances, especially for borrowers with less-than-perfect credit.

- Mortgages: Home loans enable buying a property. Co-signers often join, like spouses or family, sharing ownership and repayment responsibility.

- Personal loans: They’re flexible, for various needs like debt consolidation or renovations. Co-signers may help those with less-than-ideal credit or income, boosting approval odds.

- Home improvement loans: For renovating or repairing homes, these loans may involve co-signers to bolster applications, particularly for larger amounts or weaker credit profiles.

- Business loans: Entrepreneurs seek financing for startups or expansions. Co-signers may assist, improving approval chances and sharing repayment responsibility.

- Medical loans: For covering healthcare costs, co-signers may be involved, aiding borrowers with credit concerns and enhancing loan approval prospects.

- Emergency loans: In urgent situations, like unexpected expenses, co-signers may speed up the process, ensuring quick access to funds.

When to Consider a Co-signer for Your Loan

If you have poor credit, insufficient income, are self-employed or have a high debt-to-income ratio, a co-signer can bolster your loan application and increase your chances of approval.

How Co-signed Loans Work

In a co-signed loan setup, both the primary borrower and the co-signer apply for the loan together. The lender evaluates the creditworthiness of both parties, with the co-signers’ strong credit often playing a crucial role in securing the loan. Once approved, both parties sign the loan agreement, indicating shared responsibility for repayment.

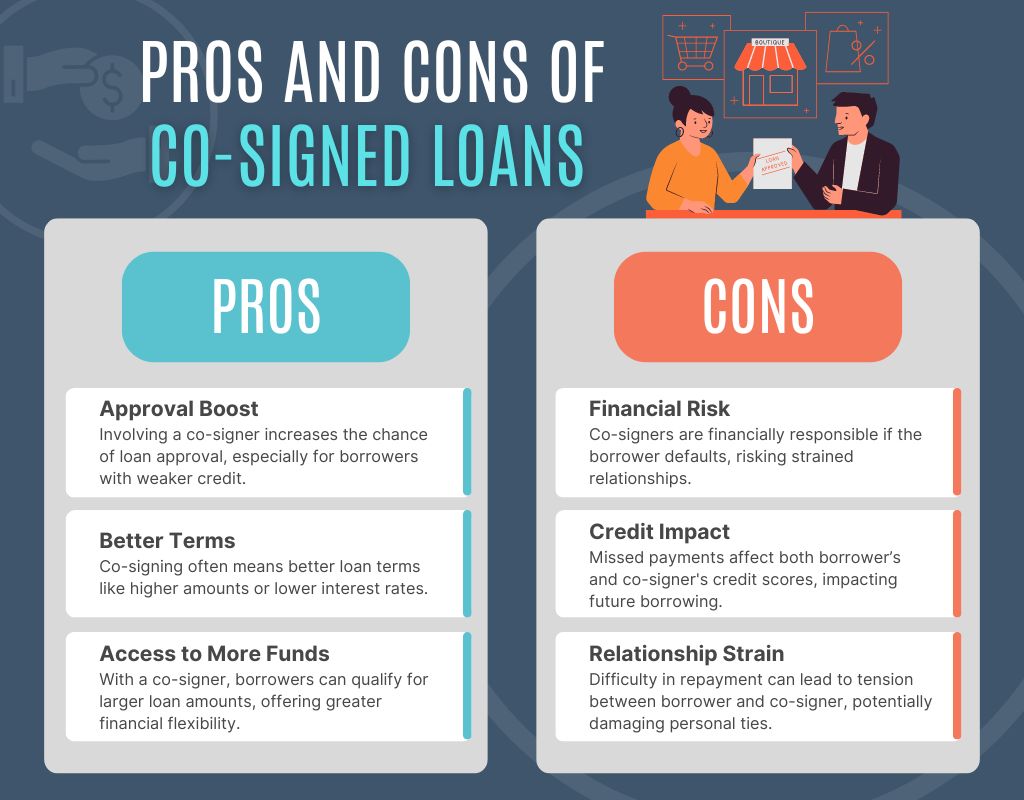

Pros of Co-signed Loans

Co-signed loans offer several advantages, particularly for the primary borrower, by expanding their financial opportunities and simplifying the borrowing process. Here are the key benefits:

1. Enhanced Approval Odds: By involving a co-signer, the likelihood of loan approval significantly increases. Lenders perceive co-signers as additional guarantees for repayment, making them more inclined to approve the loan application, especially for borrowers with weaker credit histories.

2. Favorable Loan Terms: Co-signing a loan often leads to better loan conditions for the primary borrower. This may include access to higher loan amounts, lower interest rates, or more favorable repayment terms. Such benefits may not have been attainable if the borrower had applied for the loan independently.

3. Access to Larger Funds: With a co-signer’s support, the primary borrower may qualify for a larger loan amount. This enables borrowers to address larger expenses or investments that require substantial funding, providing greater financial flexibility and capability to meet their needs.

Cons of Co-signed Loans

While co-signed loans offer advantages, it’s crucial to consider potential drawbacks before proceeding:

1. Co-signer’s Financial Risk: Co-signers bear a significant financial risk when agreeing to co-sign a loan. If the primary borrower defaults on payments or fails to fulfill their financial obligations, the co-signer becomes liable for repaying the loan. This could lead to strained relationships or financial difficulties for the co-signer.

2. Impact on Credit Scores: Both the primary borrower’s and the co-signer’s credit scores are affected by the loan’s performance. Missed payments or defaults can negatively impact both parties’ credit ratings, potentially limiting their future borrowing options and increasing borrowing costs.

3. Strained Relationships: Co-signed loans may strain relationships between the primary borrower and the co-signer, particularly if there are difficulties in repayment or disagreements regarding financial responsibility. This can lead to tension, conflicts, and potential damage to personal relationships.

Conclusion

In conclusion, co-signed loans serve as a valuable tool for individuals looking to build or rebuild their credit. By understanding how co-signed loans work, their impact on credit scores, and the responsibilities involved, borrowers can make informed decisions to achieve their financial goals and enhance their creditworthiness.

In the next articles, we’ll explore the application process for co-signed loans and strategies for managing them effectively.