Your credit report is a window into your financial world. Like any window, you want to make sure that it’s clean. You need to clear up any stains – inaccuracies, and errors in your records so lenders and creditors can get a good view of your creditworthiness. Addressing these errors is an integral part of the credit repair process.

In this chapter, we’ll embark on the credit repair journey. Credit repair is a process that involves identifying errors in your credit report, disputing inaccurate information, and crafting effective dispute letters. Let’s dive into the steps that can help you achieve a more accurate and favorable credit profile.

Identifying Errors and Inaccuracies

To correct any issues on your credit report, you need to identify them. Errors and inaccuracies are quite common. According to an investigation conducted by Consumer Reports in 2021, 11% of the study participants found errors in their personal information.

While that can present inconveniences down the line, the more worrying number is the 29% that found mistakes in their account information. These errors and inaccuracies can range from incorrect account information to improperly reported late payments or even accounts that don’t belong to you. These can negatively impact your credit scores and block important financial opportunities.

That is why regularly monitoring and thoroughly reviewing your credit report is a must. These are the first steps toward identifying these discrepancies.

As you review your report, look for:

- Incorrect Personal Information: Check for inaccuracies and misspellings in your name, address, Social Security number, and other identifying details.

- Account Errors: Review each credit account to ensure that the account type, balance, payment history, and status are accurately reflected.

- Late Payments: If your report shows late payments, check that all reported incidents are accurate. Note the correct payment date if you see any incorrectly reported late payments. You will need this information for your dispute letter.

- Accounts You Don’t Recognize: It is ideal to have your receipts and records with you as you check your accounts report. Note down any accounts that you don’t remember opening. That could be signs of identity theft or reporting errors.

- Duplicate Accounts: Ensure that accounts aren’t duplicated on your report. This error can lead to an inflated debt amount.

Disputing Incorrect Information

Once you’ve identified inaccuracies in your credit report, it’s time to take action. The Fair Credit Reporting Act (FCRA) gives you the right to dispute inaccurate information on your credit report. You can dispute errors directly with the credit reporting agencies or with the entities that provided the incorrect information (e.g., lenders, creditors).

Here’s how to initiate a dispute:

- Gather Evidence: Collect any supporting documents to prove the inaccuracies. This could be payment records, account statements, copies of correspondence with creditors, or any other relevant documents.

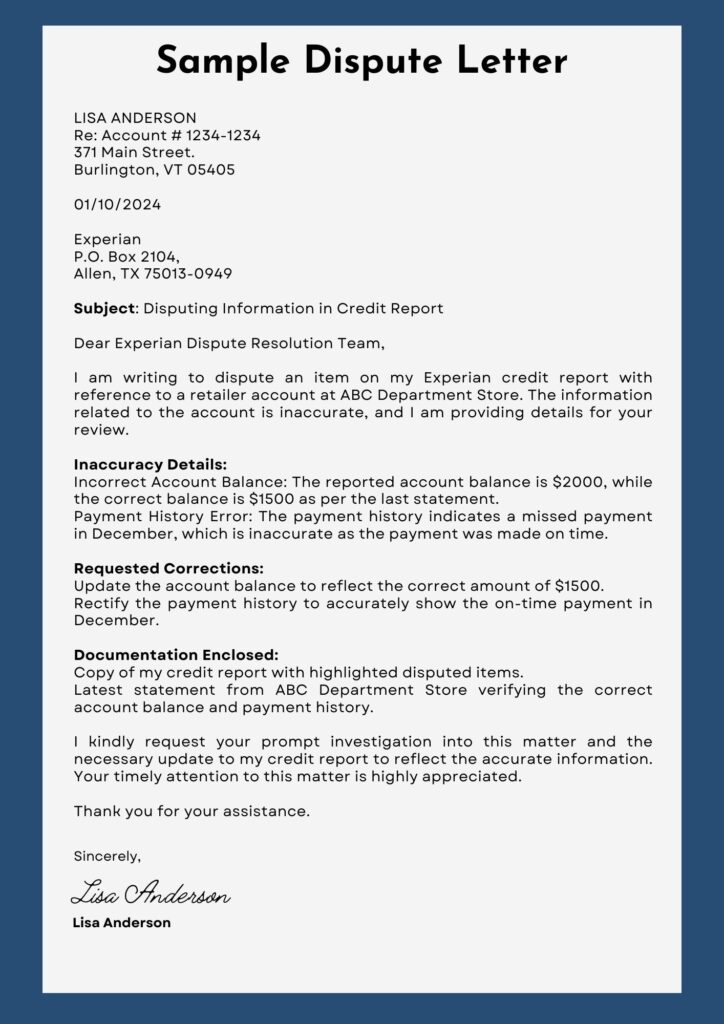

- Prepare a dispute letter: Write a letter to the credit bureau that reported the error, explaining what is wrong and why. Include your name, address, and copies of the supporting documents along with a copy of the credit report with the errors highlighted.

- Mail the letter: Send your dispute letter along with the other documents to the credit bureau by certified mail. Make sure to keep a copy of everything that you sent. You may follow up with the credit bureau after 30 days.

- Submit a Dispute Form Online: Many credit reporting agencies also offer online dispute forms. Fill up the forms and attach the necessary supporting documents then submit your dispute electronically.

Writing Effective Dispute Letters

An effective dispute letter is essential to ensure that all of your concerns are properly addressed. Here are some tips for writing a persuasive dispute letter:

- Be Clear and Specific: Clearly state the errors you’re disputing. Provide all necessary details to avoid further confusion.

- Include Evidence: Attach copies of any relevant documents that support your dispute.

- Be Polite: Maintain a respectful tone in your letter, even if you’re frustrated by the inaccuracies.

- Request Action: Clearly state that you’re requesting an investigation into the inaccuracies and the removal of any incorrect information.

- Keep Records: Make copies of your dispute letter and any supporting documents for your records. Keep the copies with you should your initial dispute letter get lost in the system. These will also be helpful when you follow up on your request.

After submitting your dispute, the credit reporting agency will investigate the matter. If they find that your dispute has merit, they’re required to correct the inaccuracy. They will then also notify the other credit reporting agencies of the correction.

Remember that the credit repair process takes time, as credit reporting agencies have a specific window within which they must investigate and respond to your disputes. Patience is key as you wait for the results of your dispute efforts.

In the next chapter, we’ll take a closer look at strategies for building positive credit habits and taking proactive steps toward improving your credit health. You’ll be able to enhance your financial well-being better by understanding the foundations of credit building.

Next: Chapter 6: Strategies for Building Positive Credit, where we’ll discuss responsible credit behaviors that can contribute to a stronger credit profile. As you implement these strategies, you’ll be on your way to achieving a more solid financial foundation.