Closing Your Secured Credit Card Account

Secured credit cards are a starting point for many looking to build or improve their credit score. There comes a time when moving on from a secured card is a smart financial move. Closing a secured credit card can be part of progressing towards financial goals, like transitioning to an unsecured credit card with better benefits. This article covers why and how to close a secured credit card, its effects on your credit score, and steps to switch to an unsecured card.

Reasons for Closing a Secured Credit Card

Deciding to close a secured credit card can be influenced by various factors, each with its own implications. Here are several reasons that may lead you to consider closing your account:

Financial Necessity

Sometimes, changes in your financial situation may necessitate accessing the security deposit tied up in a secured credit card. This could be due to unexpected expenses or shifting financial priorities. Closing the secured card allows you to use the deposit to address urgent financial needs.

Inadequate Credit Improvement

If your secured credit card fails to improve your credit score as expected, or if your score suffers due to missed payments or high utilization, it may not be serving its intended purpose. Financial strain leading to late payments can inadvertently harm your credit instead of helping it. In this case, it is more practical to just close the account to prevent it from doing more harm to your credit health.

Dissatisfaction with Your Current Issuer or Credit Card’s Performance

Dissatisfaction with the card issuer’s services or the card’s performance can also drive the decision to close a secured credit card. If customer service is lacking or if the card no longer meets your expectations, exploring other options can lead to greater satisfaction and potentially more advantageous credit terms.

Graduating to Better Products

As your financial circumstances improve, you may find that a secured credit card no longer meets your needs. Seeking features typically unavailable with secured cards, such as higher credit limits, lower interest rates, or rewards programs, could prompt you to close the secured card and transition to an unsecured card with better terms.

Steps to Close a Secured Credit Card

Closing a secured credit card involves a few crucial steps to ensure the process is smooth and does not negatively impact your financial health. Here are the key actions you should take:

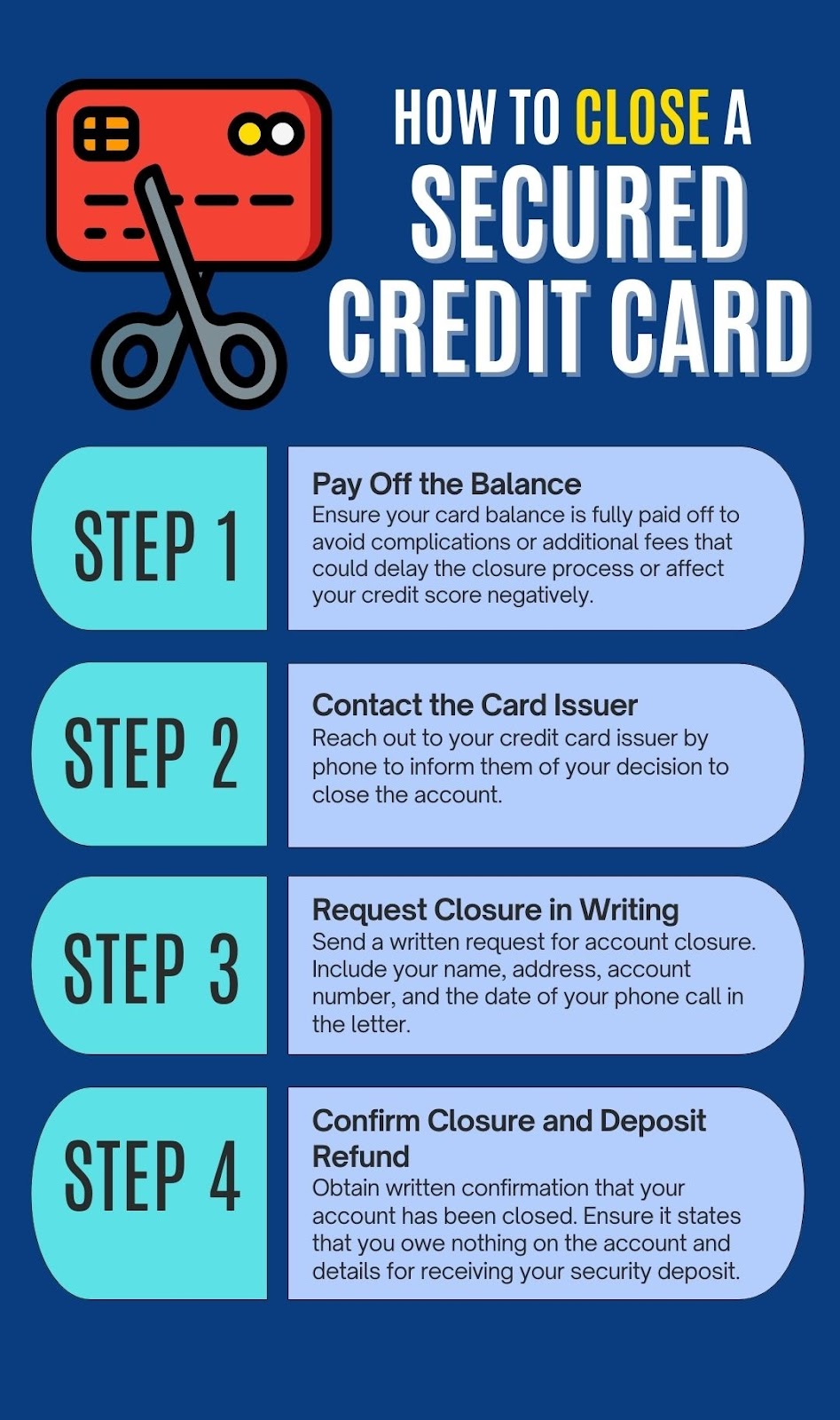

1. Pay Off the Balance

Before initiating the closure, ensure that your card balance is fully paid off. This step is essential to avoid any complications or additional fees. If you carry a balance, the closure process might be delayed or negatively affect your credit score.

2. Contact the Card Issuer

Reach out to your credit card issuer to inform them of your decision to close the account. It’s advisable to do this over the phone for immediate feedback and clarification of any steps you need to undertake. This conversation is also an opportunity to inquire about any remaining balance, fees, or the refund process for your security deposit.

3. Requesting Closure in Writing

After notifying your issuer via phone, follow up with a written request for your account closure. This step provides a record of your request and the date it was made. Include information like your name, address, account number, and the date of the phone call in your letter. Request confirmation of the account closure and the return of your security deposit in your correspondence.

4. Confirm Closure and Security Deposit Refund

After your account is closed, obtain a written confirmation from the card issuer. This document should confirm that your account is closed and that you owe nothing on the account. Also, confirm the process and timeline for receiving your security deposit refund. It’s important to keep all documentation related to the account closure and refund of your deposit for your records.

Transitioning to an Unsecured Card

Moving from a secured to an unsecured credit card is a significant milestone in your credit journey, offering numerous benefits and opportunities for financial growth. Here’s how to navigate this transition successfully:

Benefits of Upgrading

Upgrading to an unsecured card often means access to higher credit limits, lower interest rates, and better rewards programs. Additionally, unsecured cards don’t require a security deposit, freeing up your funds for other uses.

Before closing your secured card, contact your current card issuer to inquire about upgrade options. Many issuers allow direct upgrades from secured to unsecured cards while keeping the same account, which can preserve the length of your credit history and positively impact your credit score.

Steps to Transition Successfully

If you are starting over with a new issuer, these are the general steps you would need to follow to transition to an unsecured credit card:

- Review Your Credit Score: Ensure your credit score has improved sufficiently to qualify for an unsecured card. Most unsecured cards require a fair to good credit score for approval.

- Research and Compare Unsecured Cards: Look for issuers or cards that fit your financial lifestyle and goals. Consider interest rates, annual fees, rewards programs, and credit limit offerings.

- Apply for an Unsecured Card: Once you’ve chosen a card, apply through the issuer you’ve chosen. If approved, you can start using your new unsecured card.

- Close Your Secured Card Responsibly: If you are moving to a new issuer, follow the steps outlined in the section on closing a secured credit card to ensure a smooth closure.

If you are availing an upgrade from the same issuer, these are the steps to a smooth transition:

- Check if you qualify for an upgrade: Before allowing a transition from a secured to an unsecured card, lenders typically look for several key indicators of credit responsibility. This includes a certain number of timely payments. Lenders want to see that you can manage your debts responsibly. Additionally, your credit score should reflect the positive credit behaviors you’ve exhibited while using your secured card.

- Request an Upgrade: Contact your card issuer to inquire about the possibility of upgrading to an unsecured card. Some issuers may automatically review your account for eligibility after a set period.

- Handle the Security Deposit: Upon graduation, your security deposit should be returned to you, either through a direct refund or applied as a credit to your account.

Maintaining Credit Health Post-Transition

After transitioning to an unsecured card, it’s important to continue practicing good credit habits:

- Keep Making Timely Payments: Continue to pay your bills on time to maintain and improve your credit score.

- Monitor Your Credit Utilization: Keep your utilization low to show that you can manage credit effectively.

- Review Your Credit Report Regularly: Check your credit report for errors and to track your progress.

Impact on Credit Score

Closing a secured credit card can have a temporary impact on your credit score. Knowing these potential effects and strategizing to minimize negative impacts is crucial for maintaining a healthy credit score.

Potential Effects of Closing a Credit Account

Credit Utilization Ratio: This is the amount of credit you’re using compared to your total available credit. Closing a card reduces your total available credit, which can increase your utilization ratio and negatively affect your score.

Average Age of Credit Accounts: Closing an older account can decrease the average age of your credit accounts, potentially lowering your credit score. The length of your credit history accounts for a significant portion of your credit score calculation.

Strategies to Minimize Negative Impact

To minimize the negative effects of closing your secured credit card account, you can follow these tips:

Pay Down Balances on Other Cards: Before closing your secured card, try to pay down balances on other credit accounts. This can help lower your overall credit utilization ratio.

Time Your Closure: If you plan on applying for a major loan (like a mortgage or auto loan), consider waiting to close your account until after the loan process. This avoids the temporary dip in your score affecting your loan terms.

Open a New Unsecured Card First: If possible, open a new unsecured card before closing your secured card. This can help replace the credit limit you’re losing, maintaining your credit utilization ratio. As always, ensure this new card reports to all three major credit bureaus for maximum impact.

While closing a secured credit card is a step forward in your financial journey, it’s important to do so thoughtfully, considering the timing and its impact on your credit score. With careful planning and strategic decision-making, you can minimize any negative effects and continue building a strong credit profile.

Conclusion

Closing a secured credit card is a significant step towards better financial health and credit. It reflects your progress and readiness for more rewarding financial products. By carefully considering the reasons to close, following the steps to do so properly, and understanding its impact on your credit score, you can smoothly transition to an unsecured card.