Securing a co-signed loan involves a meticulous process that requires careful consideration and understanding of various factors. In this section, we’ll explore the steps involved in the application process for co-signed loans, along with essential considerations such as choosing the right lender and co-signer.

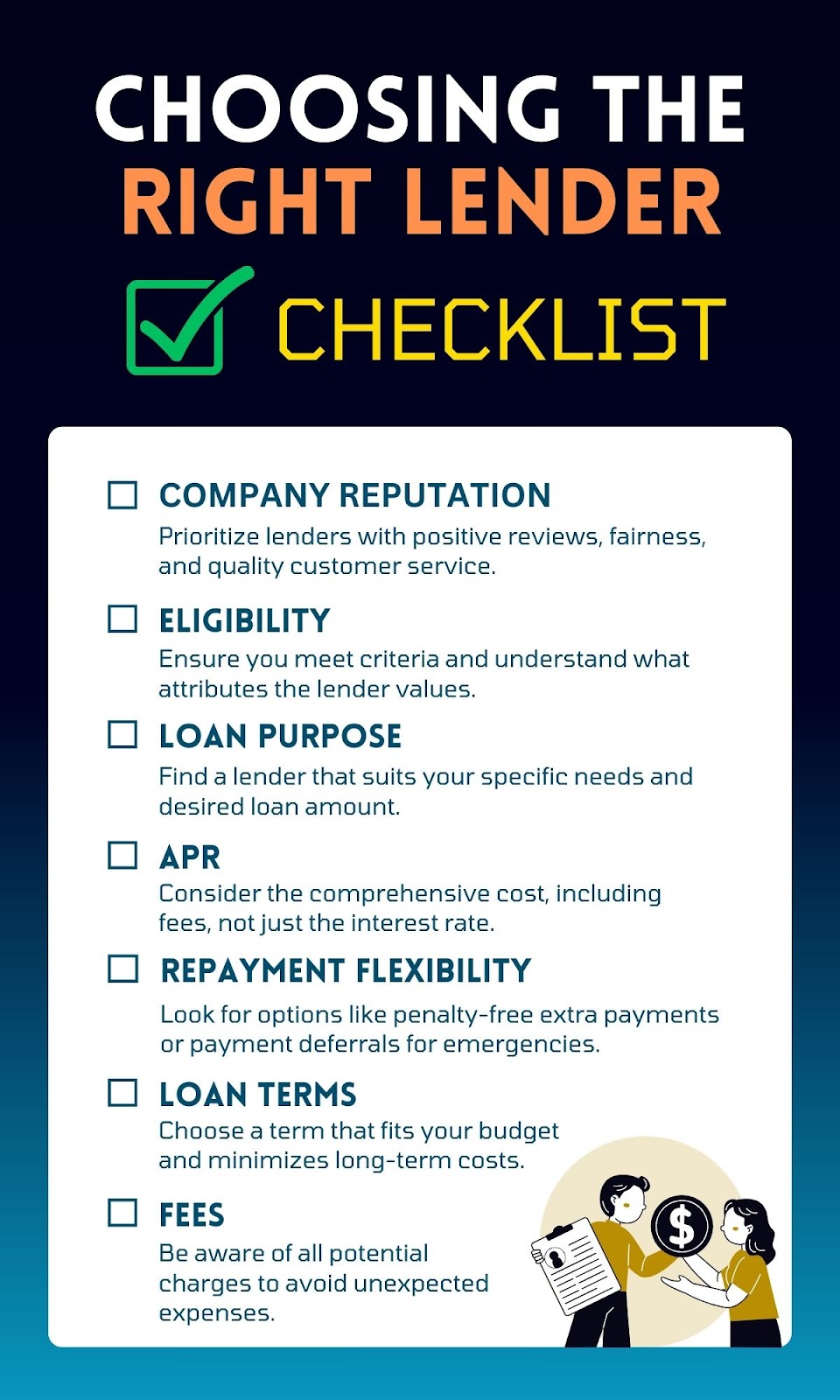

Choosing the Right Lender

Before diving into the application process, it’s crucial to research and evaluate potential lenders. Consider factors such as:

Lender Reputation

You want to ensure you’re dealing with a lender with positive reviews and is known for fairness and quality customer service.

A reputable lender is more likely to offer you a loan that’s beneficial to you, not just to them. You should choose a lender that values customer satisfaction, is more transparent about fees, and is willing to work with you to ensure you gain the credit boost you aim for.

Look beyond just star ratings; read through customer testimonials, check out forums, and even consider any awards or recognitions the lender has received.

Eligibility Requirements

It is important to verify whether you meet the lender’s criteria before getting too invested in the possibility of a loan. This is not just about whether you qualify, but also about understanding the attributes the lender values in a borrower.

Some lenders may prioritize credit scores, whereas others might emphasize income level or debt management strategies (like debt-to-income ratios).

Loan Purpose and Amount

The objective is to find a perfect fit. Not every lender is willing to finance every type of expenditure. Certain lenders offer specialized loans tailor-made for specific needs, such as home renovation or debt consolidation.

The amount you intend to borrow is equally critical. It involves finding a balance where the lender’s offerings meet your borrowing needs, ensuring you do not borrow too little and fall short, or too much and bear the burden of unnecessary debt.

APR (Annual Percentage Rate)

This is a critical factor to consider. While the interest rate indicates the basic borrowing cost, the APR incorporates any additional fees, offering a comprehensive cost overview.

This element is vital as a loan with a low interest rate but substantial fees might ultimately be more costly than a loan with a marginally higher interest rate but lower fees.

Loan Terms

Loan Terms significantly impact your financial well-being. They determine the loan’s repayment duration, which influences your monthly payments and the total interest paid throughout the loan’s life.

A longer term might reduce monthly payments but increase the total interest, whereas a shorter term entails higher monthly payments but decreases the total interest cost over time.

The goal is to find a term that suits your monthly budget without incurring excessive long-term costs.

Fees and Charges

Fees and Charges represent potential unforeseen expenses in your loan agreement. This category includes origination fees, late payment fees, and prepayment penalties, among others, which can unexpectedly elevate your loan’s cost.

For example, a prepayment penalty could penalize you for settling your loan early. Thus, it is essential to inquire about all possible fees before the agreement is finalised.

Repayment Flexibility

Repayment Flexibility offers a safety net amidst life’s unpredictability. Options such as making additional payments without penalties, altering your payment date, or even deferring a payment during emergencies can provide significant relief.

This flexibility ensures that your loan can accommodate fluctuations in your financial situation without exacerbating financial challenges.

Choosing a Co-signer

Choosing the right co-signer is just as crucial as picking the right lender for your loan. It’s not just about finding someone who’s willing; it’s about making sure they’re a good match. Here’s what you should consider when looking for the perfect co-signer:

- Creditworthiness: Look for a co-signer with a strong credit history and a good credit score. Lenders typically prefer co-signers who have a proven track record of responsible financial behavior. The credit score required for a cosigner to be considered for a loan is generally around 670 or better, which falls within the range of very good to excellent credit

- Trust and Reliability: Choose someone you trust and who trusts you. Co-signing a loan is a significant responsibility, and it’s essential to have a reliable co-signer who understands the commitment involved.

- Financial Stability: Ensure that your co-signer has stable income and financial stability. They should be able to comfortably cover the loan payments if you are unable to do so.

- Willingness to Co-sign: It’s essential to have open and honest communication with your potential co-signer. Make sure they understand the risks and responsibilities associated with co-signing a loan and are willing to take on this role.

- Relationship Dynamics: Consider the dynamics of your relationship with the potential co-signer. Co-signing a loan can strain relationships, so it’s essential to choose someone with whom you have a strong and trusting relationship.

- Legal Capacity: Ensure that your co-signer meets all the legal requirements to co-sign a loan. They should be of legal age and have the legal capacity to enter into a binding contract.

The Application Process for Co-signed Loans

Once you’ve selected a suitable lender, follow these steps to apply for a co-signed loan:

- Choose a Co-signer: Select a trusted individual with a strong credit history to co-sign the loan with you.

- Check Credit Scores and Financial Information: Review both your and your co-signer’s credit scores, incomes, and debt-to-income ratios to set expectations.

- Research: Compare loan features and requirements from multiple lenders to find the best fit for your needs.

- Pre-Qualify and Add a Co-Applicant: Begin the application process by pre-qualifying with prospective lenders. Provide necessary personal and financial information for both parties.

- Submit Application and Receive Funds: After completing the application process, the lender will conduct a hard credit check on both applicants. If approved, expect to receive funds within a few days.

Finalizing the Loan

Securing approval for a loan is undoubtedly a significant milestone in the borrowing process. However, it’s crucial to recognize that approval isn’t the end of the journey. There are still essential steps to take to tie loose ends and ensure a smooth transition towards finalizing the loan.

- Read and Understand the Agreement: Carefully examine the terms of the loan, including the interest rate, repayment schedule, and any associated fees.

- Ask Questions: Seek clarification from the lender on any aspects of the agreement that are unclear or require further explanation.

- Sign the Agreement: Once satisfied with the terms, the borrower and the co-signer must sign the loan agreement to proceed.

- Disbursement: Upon signing, the loan amount will be disbursed according to the terms of the agreement.

By following these steps and considerations, borrowers can navigate the application process for a co-signed loan effectively, increasing the likelihood of approval for both themselves and their co-signers.

Conclusion

Knowing how to find the right lender and co-signer, coupled with having a clear understanding of the application process, significantly contributes to a smoother experience.

Looking ahead, the next steps involve managing and maximizing the loan effectively to reap its benefits fully. In the forthcoming article, we’ll delve into strategies for managing co-signed loans to boost your credit score and establish a stable credit history. By implementing these strategies, borrowers can achieve their financial goals with confidence and resilience.