Tackle the widespread myths and misconceptions about credit reports head-on, clarifying common confusions and setting the record straight for informed credit management.

Understanding credit reports can be challenging due to the prevalence of misconceptions. These erroneous beliefs can lead individuals astray when navigating their financial management.

It is imperative to dispel these misconceptions to empower individuals to make informed financial decisions and safeguard their financial well-being.

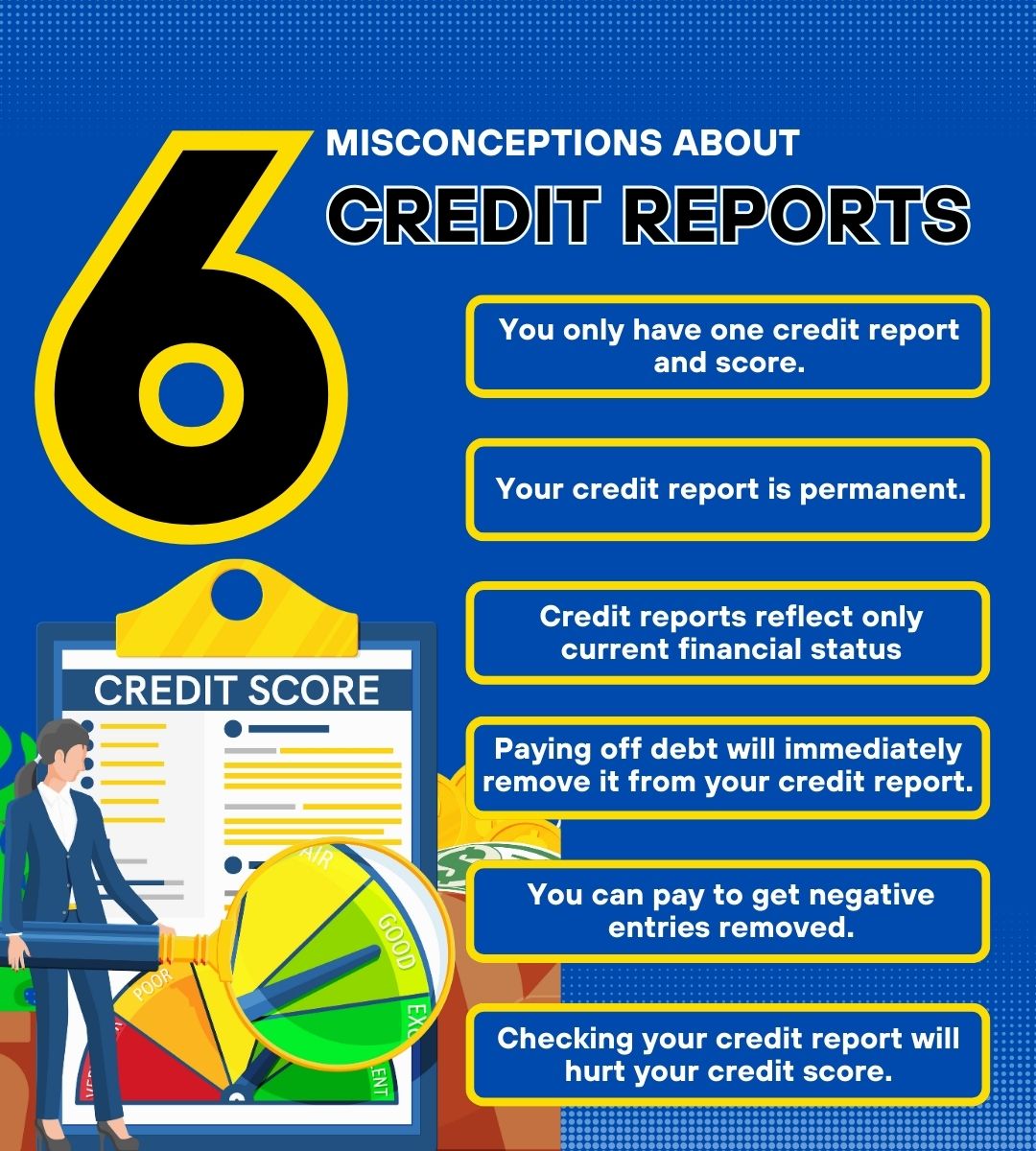

1. You Only Have One Credit Report and Score

Many believe they have a single, definitive credit report and score. However, in reality, there are numerous scoring models used by lenders, such as FICO and VantageScore.

Additionally, each of the three major credit bureaus—Equifax, Experian, and TransUnion—compiles its own credit report, leading to potential variations in scores.

Understanding these differences empowers you to be proactive in managing your finances. For instance, if a specific lender relies on one particular credit report for their decision-making process, you can investigate the scoring model used by that bureau and take action to potentially boost your credit score before applying.

2. Your Credit Report Is Permanent

Many individuals mistakenly believe that the information on their credit report is set in stone and cannot be altered. This misconception can lead to a sense of resignation, as people may feel powerless to address any errors or inaccuracies that could be harming their creditworthiness.

However, the truth is far from static – your credit report is dynamic and constantly evolving.

Every financial move you make, from paying bills on time to opening new lines of credit, is tracked and reported by banks, stores, and even your landlord. These actions have a direct impact on your credit report, influencing your credit score for better or worse.

Understanding this dynamic nature empowers individuals to take proactive steps in managing their financial reputation.

By making responsible financial decisions and regularly monitoring your credit reports, you can ensure that your creditworthiness accurately reflects your financial habits and responsibilities.

3. Credit Reports Reflect Only Current Financial Status

Some individuals mistakenly believe that credit reports only contain information about their current financial status and activities. This misconception can lead to overlooking the importance of past financial behaviors and their impact on creditworthiness.

In reality, credit reports often include historical data, such as past credit accounts, payment history, and derogatory marks, which can influence credit scores and lending decisions.

4. Paying Off Debt Will Immediately Remove It From Your Credit Report

While paying off debts in collections is a positive step, it doesn’t automatically remove the debt from your credit report. Most negative information, such as late payments and collections, can stay on your report for up to seven years, even if you’ve paid off the debt.

However, past mistakes or financial setbacks shouldn’t discourage you. Despite negative entries remaining on your credit report for a period of time, their impact lessens over time, especially as you demonstrate responsible financial behavior.

By continuing to make timely payments and practicing good credit habits, you can gradually rebuild your creditworthiness and improve your financial standing.

5. You Can Pay to Get Negative Entries Removed From Your Credit Report

There is a misconception that negative entries, such as late payments or collections, can be removed from your credit report by paying a fee to credit repair companies.

In reality, credit repair companies cannot remove accurate and verifiable information from your credit report.

Legitimate negative entries can only be removed through the dispute process if they are inaccurate or outdated.

Moreover, if a credit repair company promises to get negative entries removed from your record in exchange for payment, it’s crucial to steer clear.

Such claims often indicate fraudulent practices, as no one can simply erase legitimate negative entries from your report.

6. Checking Your Credit Report Will Hurt Your Credit Score

Some individuals avoid checking their credit reports because they fear it will negatively impact their credit scores. However, this belief is a common misconception.

In reality, checking your own credit report is considered a “soft inquiry” and does not affect your credit score. It’s solely for informational purposes, allowing you to review your credit history and ensure its accuracy.

On the other hand, “hard inquiries” occur when lenders or creditors check your credit report as part of a credit application process. This takes place when you apply for a loan or credit card. These inquiries can have a temporary impact on your credit score, but the effect is typically minimal and short-lived.

Bottom Line

Demystifying these common misconceptions about credit reports is vital for anyone looking to improve their financial literacy and health.

Knowing the facts empowers you to take control of your credit, make informed decisions, and navigate your finances confidently. Remember, your credit report is a valuable tool for your financial well-being. Make sure to utilize it wisely and regularly.