In the quest to elevate your credit score, credit builder loans emerge as a potent ally. Yet, harnessing their full potential requires more than just a surface-level understanding. To truly benefit from what they offer, it’s crucial to dive deep into the mechanics, benefits, and strategic use of these financial tools. Here, we’ve prepared a comprehensive credit builder loans FAQ section that aims to demystify the financial product for you.

From the basic how-tos to more complex inquiries about their impact on your credit history, we’ve tackled the essential questions to ensure you’re thoroughly equipped with the knowledge needed to make these loans work in your favor.

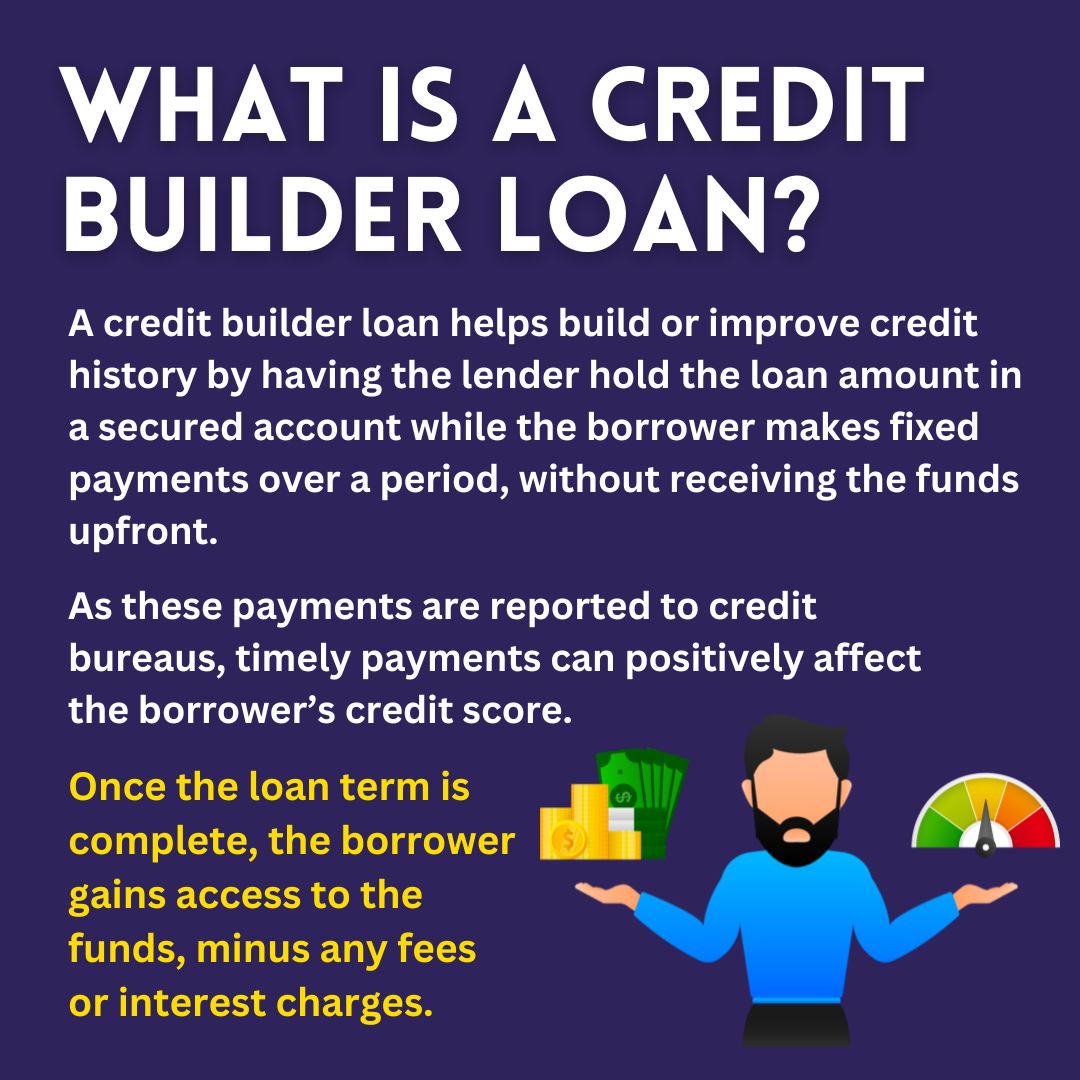

What is the difference between a credit builder loan and a personal loan?

A Credit Builder Loan is aimed at improving your credit score. The loan amount is locked away by the lender while you make payments towards it; you access the funds after fully paying the loan. In contrast, a personal loan gives you immediate access to funds for various personal uses, with repayment over time based on the agreed terms.

How much can I borrow with a credit builder loan?

Credit Builder Loans typically range from $300 to $3,000, depending on the lender. It’s important to assess your financial situation and choose a loan amount that fits your budget.

What is the payment period for Credit Builder Loans?

Repayment terms for Credit Builder Loans usually span from 6 to 24 months. Borrowers make fixed monthly payments into an account until the loan term ends, after which they gain access to the loan funds.

What are the interest rates for Credit Builder Loans?

The Annual Percentage Rate (APR) for Credit Builder Loans generally falls between 6% and 16%, making them a cost-effective option for building credit.

Can I access the loan amount before repayment?

No, the loan amount is only accessible once all payments are made or the loan term ends. This feature ensures responsible repayment behavior and helps build credit

Are there fees associated with Credit Builder Loans?

Yes, there may be fees like account opening fees or administrative costs. It’s important to review and understand all terms, including fees and interest rates, before committing to a Credit Builder Loan.

What should I look for in a Credit Builder Loan?

For a credit builder loan, look for low interest rates and minimal fees, a manageable loan amount and repayment schedule, reporting to all three major credit bureaus, and additional features like financial education resources.

How long does the application process take for a Credit Builder Loan?

The application process for a Credit Builder Loan can vary depending on the lender. Some lenders offer quick online applications with instant decisions, while others may take a few days to process and approve the loan.

What are the minimum requirements for a credit builder loan?

To qualify for such a loan, applicants generally need to meet certain criteria, including being at least 18 years of age, possessing a valid government-issued ID, having a bank account, and providing proof of stable income to ensure repayment capability. A Social Security Number is also required for credit reporting purposes. Specific requirements can vary by lender, so it’s advisable to consult directly with the financial institution offering the loan.

Can I be denied a Credit Builder Loan?

It is possible to be denied a credit builder loan, just like any other type of loan. While having poor credit or no credit history may not necessarily lead to denial, insufficient proof of income could be a reason for rejection.

Will applying for a Credit Builder Loan negatively affect my credit score?

Most lenders perform a soft credit check when you apply for a Credit Builder Loan. This type of inquiry does not impact your credit score. However, once approved, late payments on the loan can negatively impact your credit history and score.

What happens if I miss a payment on a Credit Builder Loan?

If you miss a payment on a Credit Builder Loan, it may negatively impact your credit score. That’s because lenders report account activity to credit bureaus. However, some lenders may offer options to negotiate a payment plan for a missed payment. Taking advantage of this can help you potentially avoid further damage to your credit score.

Conclusion

Credit builder loans are a helpful instrument for establishing or improving credit scores. By making timely payments and understanding the specifics of how these loans function, you can effectively enhance your credit profile. Understanding the ins and outs of your credit builder loan is vital to making an informed financial decision and applying with confidence.