Your credit report may be viewed as your financial report card. It describes in detail your financial path and offers an analysis of how successfully you’ve handled your money thus far. This report is an invaluable tool for assessing your creditworthiness.

Credit reports contain a lot of information, from your personal details to your account history and potential red flags. In this chapter, we will look into the different sections to better understand the story that your credit report tells.

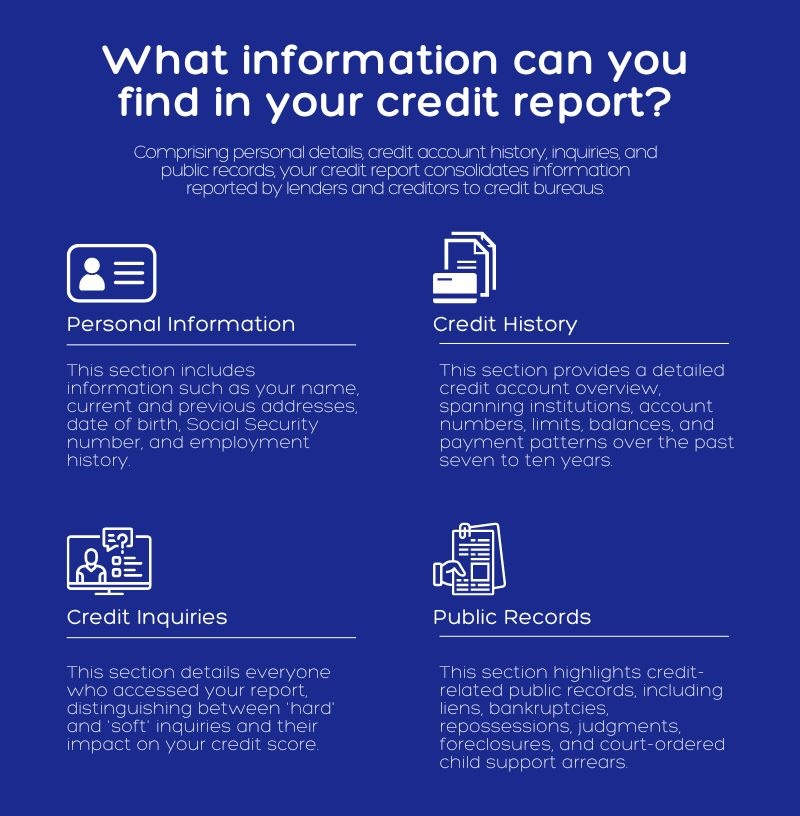

What’s in your Credit Report?

The information in your credit report can be broken down into four sections: personal information, credit account history, credit inquiries, and public records. Understanding what each section contains can help you read your credit report and identify any potential errors or discrepancies.

Personal Information and Identifying Details

At the top of your credit report, you will find your personal information. This section is important because it verifies that the data contained in the report is authentic and correctly linked to your credit history.

It is important to check this part for inconsistencies or inaccuracies since any error here may have an impact on your credit profile. Making sure that the information in this section is accurate can also protect you from fraudulent activities such as identity theft.

Key elements and what you need to check:

- Name and Aliases: Check if your name is spelled correctly and that any known aliases or variations are accurate.

- Address: Check to see if your current and previous addresses are listed accurately.

- Social Security Number: Verify that your Social Security number is correctly entered.

- Date of Birth: Make sure your birthdate is accurate.

- Employment Information: Some reports might include employment history or current employment information.

Account History: Credit Cards, Loans, Mortgages, etc.

The account history is the heart of your credit report. It provides a detailed record of all your credit accounts, showing how you’ve managed them over time. This section should cover open accounts as well as those that have been closed within the last 7 – 10 years.

Key elements and what you need to check:

- Account Type: All of your accounts will be presented according to these categories: revolving (credit cards and other lines of credit), installment (fixed-payment debts), mortgage, and others (child support and other legally required financial obligations). Make sure that the details are all correct.

- Account Status: Check if the account is correctly marked as open, closed, or in collections.

- Account Balance: This includes information like your original loan amount, payments made, and outstanding debt. Make sure to check the current balance on the account.

- Payment History: This presents a record of your payment behavior. It lists down all of your on-time payments, late payments, and any missed payments.

- Credit Limit/Original Loan Amount: For credit cards or other lines of credit, this section shows the maximum amount you can borrow. For loans, it represents the initial loan amount. Verify if the numbers match your records.

Credit Inquiries

This section presents entries that appear whenever a legally authorized entity accesses your credit information. We can categorize them as soft or hard inquiry.

Key elements and what you need to check:

- Hard Inquiries: Entries appear whenever you apply for credit, loans, goods, or services. These stay on your report for a few years and impact your credit score. Note that accumulating too many hard inquiries can lower your score temporarily. Check the recognitions of the lenders and institutions that conducted the inquiries.

- Soft Inquiries: Entries appear whenever someone runs a credit check on you. It could be for whenever you check your credit report. It is also commonly used for pre-approval by creditors. This type of inquiry does not have any impact on your credit score.

Public Records and Collection Accounts

This section contains information about any public records directly related to your credit history. They will remain on your record for 7 – 10 years and can have a huge impact not only on your score but also on your overall financial reputation.

Key elements and what you need to check:

- Bankruptcies: If you have filed for bankruptcy, it will be listed here. Note that the entries for the type and date of the bankruptcy are accurate. If the bankruptcy is older than 10 years but is still in your report, you should dispute it.

- Tax Liens: Any unpaid tax obligations might appear as a tax lien on your credit report.

- Civil Judgments: Entries here include any instance when a court has ruled against you in a civil case involving financial matters.

- Collection Accounts: This is a record of any account that collections receive due to non-payment.

These entries can have a lasting impact on your credit score and can take time to recover from. You have the right to dispute any of the items that are inaccurate or unfair.

Getting to know the different sections of your credit report will give you a better idea of how lenders perceive your financial behavior. In the next chapter, we’ll continue learning more about credit inquiries and how they can impact your credit profile.

Next: Chapter 4: Understanding Credit Inquiries, where we’ll take a closer look at credit inquiries. By knowing the ins and outs of credit inquiries, you’ll have a better understanding of how they can impact your credit score and be better equipped to manage your credit health effectively.