Your credit score: it’s that magical number that opens or closes doors to financial opportunities. But what goes into that three-digit figure that has such a big impact on people’s lives? Understanding the factors that affect your credit score isn’t just useful—it’s essential for anyone looking to secure a better financial future.

Here, we’ll dissect the five key elements that make up your credit score, offering not only insights but also real-life strategies to enhance your financial standing.

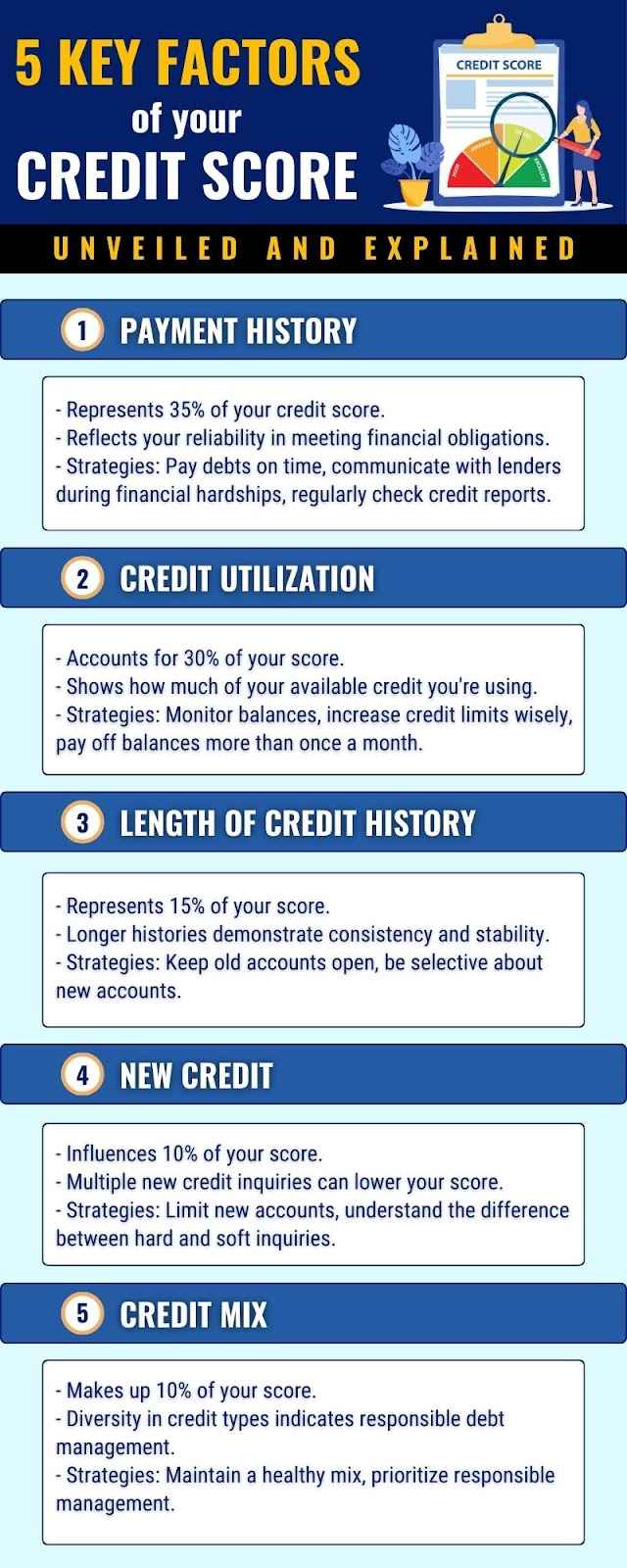

Payment History: The Backbone of Your Credit Score

Understanding how you’ve managed your debt in the past can provide valuable insights for lenders when assessing your creditworthiness.

Your payment history stands as the backbone of your credit score, wielding immense influence as it constitutes a substantial 35% of the score. Essentially, it serves as a mirror reflecting your reliability in meeting financial obligations, thereby enabling lenders to gauge the risk associated with extending credit to you.

This critical aspect of your credit score scrutinizes your promptness in paying bills, encompassing credit cards, loans, and various other debts. Late payments, defaults, bankruptcies, and other adverse marks can significantly dent your score, signaling to lenders potential risks in extending credit to you.

Each late payment or, worse, missed payment acts as a red flag, suggesting a propensity for repeating such behavior in the future.

Consequently, lenders may choose to approve your application, reject it outright, or offer you credit at a higher interest rate to mitigate the perceived risk.

Real-Life Strategy: Keeping Your Payment History Spotless

- Pay your debts on time: Mark your calendar with due dates or set up automatic payments to ensure you never miss a deadline.

- Communicate with lenders if you’re facing financial hardships: Many creditors offer hardship programs that can adjust your payment plan in times of need.

- Regularly check your credit report: This can help you spot and dispute any inaccuracies that could unfairly affect your payment history.

Credit Utilization: Less is More

Your credit utilization ratio, which shows how much of your available credit you’re using, accounts for 30% of your score. A lower ratio signals to lenders that you’re not overly reliant on credit to meet your financial needs, which positively impacts your score.

In simpler terms, it indicates that you’re either earning enough income to pay for your purchases without relying heavily on credit, or you’re not spending beyond what you can afford to pay back.

Credit utilization is calculated by dividing your total credit card balances by your total credit limits. The sweet spot for maintaining a good score is using less than 30% of your available credit.

This means you’re not maxing out your credit cards or relying heavily on loans, which can indicate responsible financial management and make you a more attractive candidate for credit approval.

Real-Life Strategy: Mastering Your Credit Balance

- Monitor your balances: Keep your credit card spending well below your limits. Regular monitoring can help you adjust your spending habits.

- Increase your credit limits: If your financial situation allows, request a higher credit limit from your card issuers—but don’t increase your spending.

- Pay off your balances more than once a month: This can help keep your utilization low, especially if you’re a heavy card user.

Length of Credit History: Time is on Your Side

Your credit history length, which accounts for 15% of your credit score, refers to how long you’ve been using credit.

Lenders prefer borrowers with longer credit histories because it gives them more data to evaluate your creditworthiness. Longer histories show consistency in payment behavior and provide stability, making lenders more confident in your ability to manage credit responsibly over time.

This factor takes into account how long your credit accounts have been open, including the age of your oldest account, the age of your newest account, and the average age of all your accounts.

Real-Life Strategy: Aging Like Fine Wine

- Keep old accounts open: Unless there’s a compelling reason to close an account (like high fees), keeping it open can lengthen your credit history.

- Be selective about opening new accounts: Too many new accounts can lower your average account age, which can negatively affect your score.

New Credit: Quality Over Quantity

New credit inquiries and recently opened accounts suggest you might be taking on more debt, potentially increasing your financial risk. This area influences 10% of your score.

Applying for several new credit lines in a short period can hurt your credit score. Each application typically involves a hard inquiry, which can slightly lower your score.

Real-Life Strategy: Slow and Steady Wins the Race

- Limit new accounts: Only apply for new credit when necessary, and try to spread out your applications.

- Understand the difference between hard and soft inquiries: Checking your own credit score is a soft inquiry and doesn’t affect your score.

Credit Mix: Diversity is Your Friend

The types of credit you have (credit cards, mortgages, auto loans, etc.) make up 10% of your score. A mix of credit types can show lenders that you can handle various debts responsibly.

While it’s beneficial to have a diverse set of credit accounts, it’s more important that you manage them well. Opening accounts you don’t need can do more harm than good.

Real-Life Strategy: Building a Well-Rounded Credit Portfolio

- Maintain a healthy mix: If it makes financial sense, having both revolving credit (like credit cards) and installment loans (like a car or student loan) can benefit your score.

- Prioritize responsible management: Always make timely payments and keep balances low, regardless of the type of credit.

Bottom Line

Understanding and optimizing these five factors can significantly influence your credit score, opening up new financial opportunities. Remember, improving your credit score is a marathon, not a sprint. It requires patience, discipline, and a proactive approach to your finances.

By integrating these strategies into your financial routine, you’re not just working toward a better credit score—you’re building a foundation for a more secure financial future.